Thursday, April 25, 2024

Fair, 70°Wind: 10.4 mph, S

Welcome to our new web site!

To give our readers a chance to experience all that our new website has to offer, we have made all content freely avaiable, through October 1, 2018.

During this time, print and digital subscribers will not need to log in to view our stories or e-editions.

Judging by the stock market, investors are starting to take the novel coronavirus seriously. As of this writing (Feb. 28), the market is down 12 percent from its all-time high two weeks before. This is bad news as the best single indicator of future economic activity. The market seems to be predicting that Covid-19, the disease caused by coronavirus is to be taken seriously

Other measures of future economic activity also are moving down. One index that predicts recessions has increased in the last month from 20 percent probability during 2020 to 40 percent. Oil prices, an import indicator for New Mexico, has seen a major sell. West Texas Crude fell below $50, the magic number underlying state budget estimates.

The fear is that attempts to contain the virus will disrupt international trade. Global markets are far more integrated today than in 2003, when another coronavirus caused the SARS outbreak. Airline travel, for example, has doubled since then and international trade has increased by a factor of three.

And yet the virus spreads, with outbreaks in Italy, Japan and elsewhere. As of this writing, the first report of an outbreak in the United States not related to international travel was reported.

We don’t know a lot about Covid-19. We do know that the virus spreads easier than its recent predecessors—SARS and MERS. Symptoms start mild. Victims, not realizing that they are sick, inadvertently expose others to infection.

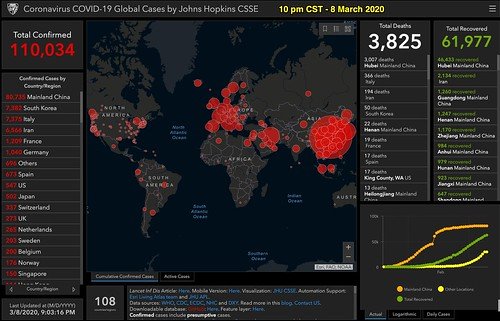

Things are changing fast, but right now, as I write, there have been about 80,000 cases diagnosed. Many patients suffer respiratory distress, with about 15 percent needing hospitalization with an average stay of about 10 days; about 3 percent dying. This is a very high morbidity and mortality, much higher than seasonal flu, for example.

On the face of it, this is very scary. If in the long run, these numbers prove to be representative of the disease, this will be the worse epidemic in our lifetimes. But here is the thing, we have diagnosed 80,000 cases but there is selection bias. Early on in a new disease, the sick who show up at the doctors’ office get diagnosed. There may be many cases that are asymptomatic or nearly asymptomatic that go undiagnosed.

If there are, in fact, a large number of undiagnosed cases, then the true morbidity and mortality rates may be much lower. But who knows? Also, our current experience comes mainly from China, where medical care is much more modest than in western countries.

Ironically, the attempts to prevent the spread of Covid-19 may be more harmful economically than the disease itself. In Peking, for example, residents are encouraged to stay at home. If they must go out, they must show a pass to their apartment door attendant to be let out, then their temperature is taken every three blocks. Trying to do business in these circumstances is difficult.

Should Covid-19 escape into the general population, which it appears to have done, efforts to quarantine and contain will be phased out as ineffective. The consequence will be a return to business as normal, although with many sick colleagues not reporting to work.

One thing we can say for sure is that there is a great deal of uncertainty about Covid-19, and markets hate uncertainty.

Christopher A. Erickson, Ph.D., is a professor of economics at NMSU. He has been at NMSU since 1987. The opinions expressed may not be shared by the regents and administration of NMSU. Chris can be reached at chrerick@nmsu.edu.